NAREB 2023 State of Black Housing Highlights

February 7, 2024

February is Black History Month, a time to celebrate the achievements and recognize the struggles that Black Americans have made in this country. Homeownership is one of those areas where Black people have made progress but are still grappling with things such as appraisal bias and exclusionary housing practices. The 2023 State of Housing in Black America report put out by the National Association of Real Estate Brokers (NAREB) focuses on these and other factors affecting Black homeownership; here are the highlights.

Black homeownership rates face challenges due to income and wealth.

Low inventory, high home prices, and mortgage rates have plagued the housing market over the last two years with most Americans needing to make $115,000 to afford a median priced home. With the median household income for Black households at $52,860 this would put home buying out of reach for many. The median net worth for Black households is also lower at $24,520, 10 times less than White households. The combination of these factors has led to little improvement in the homeownership rate which was 45.9% in the fourth quarter of 2023, up just 2.7% in the last decade.

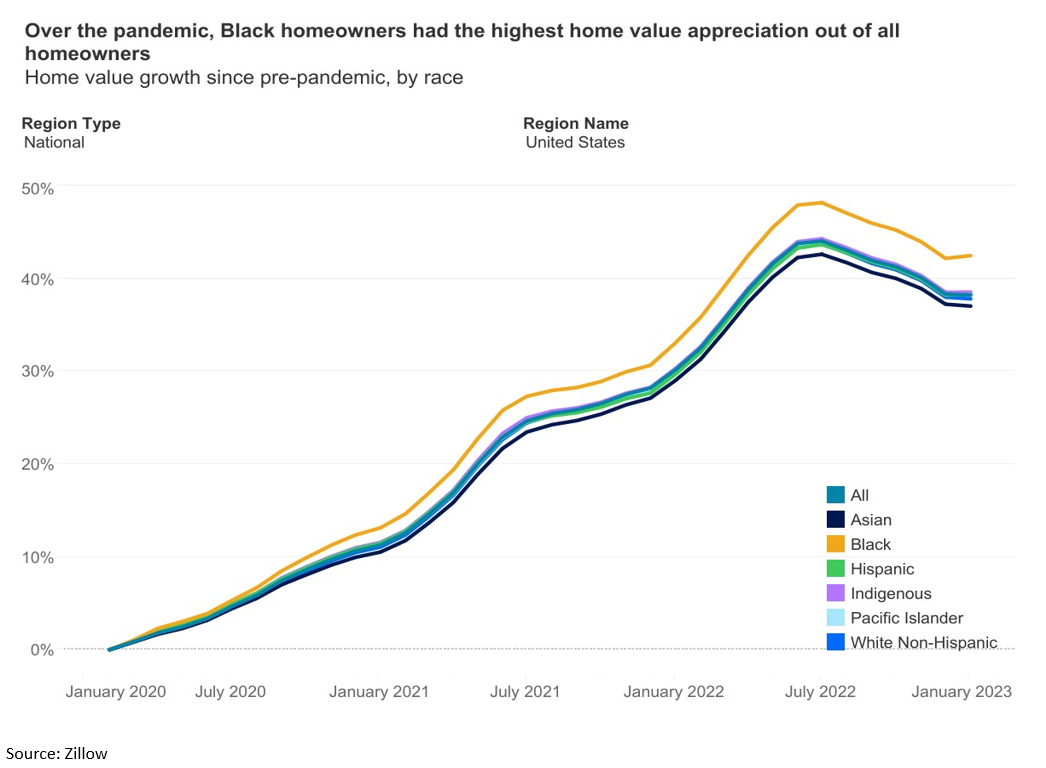

Home values grew but disparities remain.

From January 2020 to 2023, Black home values rose 42.5%, the fastest growth across all races and ethnicities. With 66% of Black households’ median net worth coming from home equity, it is a positive sign but there is still great disparity when it comes to Black neighborhoods. The report found that homes located in predominantly Black neighborhoods are valued 21-23% below homes in non-Black neighborhoods. These homes are also 1.9 times more likely to be appraised under the contract price than homes located in majority-White neighborhoods.

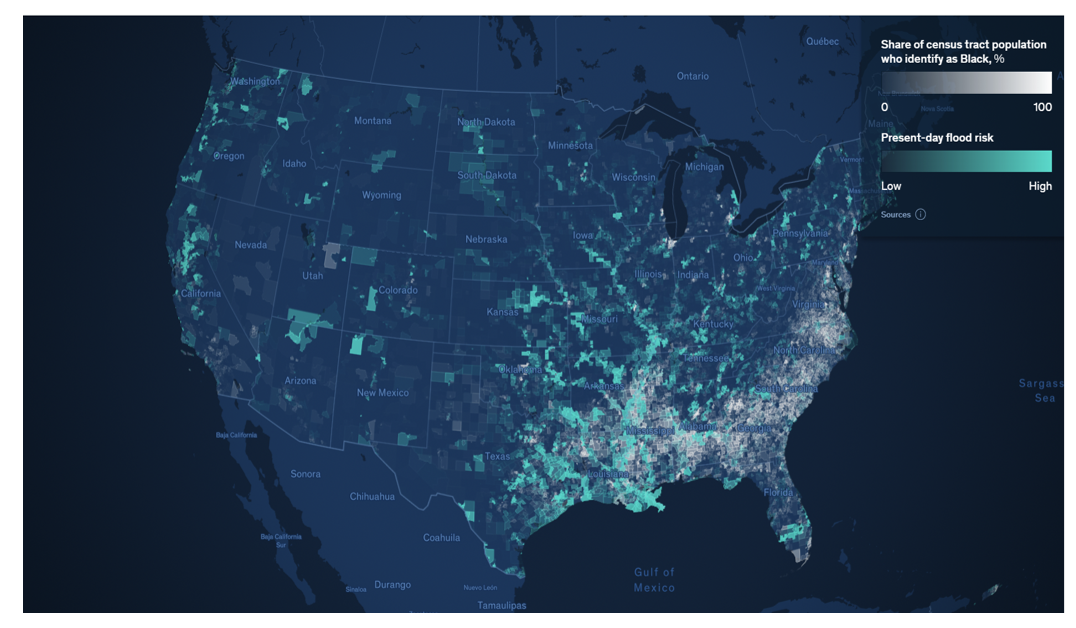

Climate change will greatly affect black neighborhoods.

Extreme weather is having a significant impact on the world with communities of color being disproportionately affected. Per the report, 19% of the Black population lives in areas that are at high risk for hurricanes and floods and 33% live in areas where they are exposed to heat waves. Bias practices such as redlining and racial steering have contributed to Black families living in neighborhoods with less vegetation and older homes that are unequipped to handle damage from natural disasters. The factors that result from climate change such as property damage, health risk, and high insurance premiums will only widen the racial inequities that these communities are already experiencing.

Source: McKinsey Institute for Black Economic Mobility

Higher credit scores, limited access to traditional financing.

Although the median credit score for Black borrowers was 695 in 2022, it is still 56 points below that of White borrowers. Limited access to credit, lack of generational wealth, and a long history of discriminatory lending practices has contributed to lower credit scores, or a lack of credit history known as credit invisibility. As a result, 40% of Black consumers have access to subprime loans which tend to have higher interest rates than prime loans. At 25%, Black households are more likely to use alternative services such as payday loans despite having a checking or savings account, being referred to as underbanked.

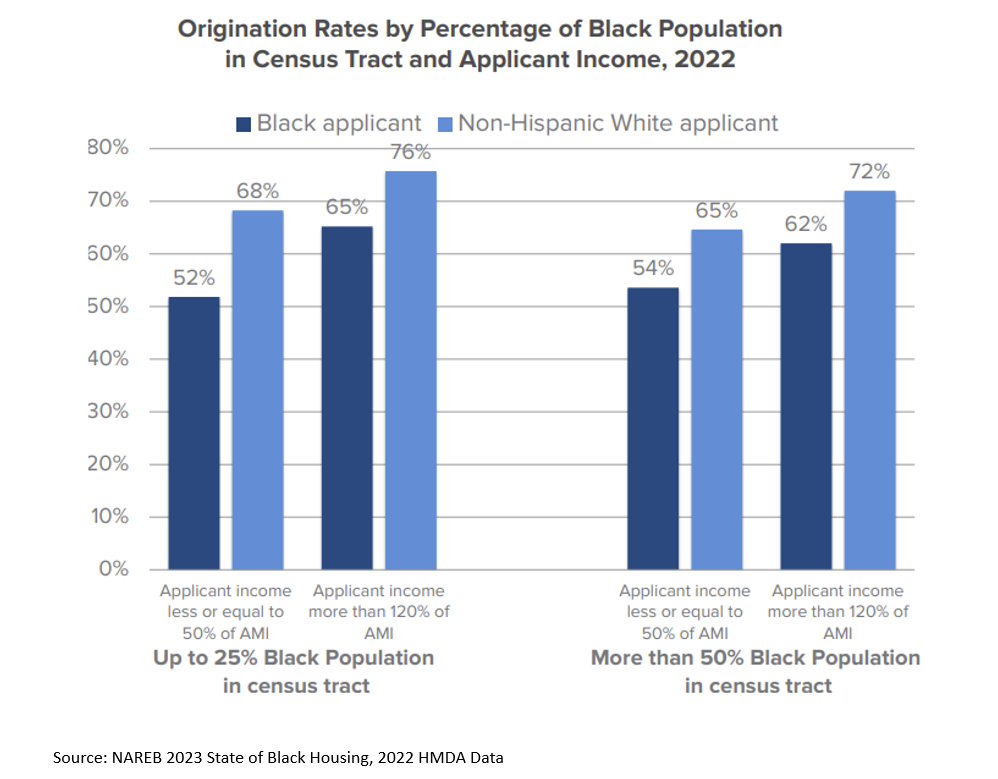

Higher denials, more originations in Black neighborhoods.

The denial rate for Black applicants was 17% in 2022, more than twice the rate of White applicants at 7%. Debt-to-income ratio was the main reason applications were denied for Black borrowers at 39%, up from 34% in 2021. The number of loans obtained for homes located in majority-minority neighborhoods was 54% for Black borrowers, up 11 percentage points from 2021. For Black applicants who had lower incomes, loan originations were higher in predominantly Black neighborhoods while high-income Black applicants had higher originations in areas with smaller Black populations.

For more information on housing, demographic and economic trends in Virginia, be sure to check out Virginia REALTORS® other Economic Insights blogs and our Data page.

You might also like…

Midway Through 2024, Virginia Home Sales Activity Slightly Outpacing Last Year

By Robin Spensieri - July 24, 2024

According to the June 2024 Virginia Home Sales Report released by Virginia REALTORS®, there were 10,018 homes sold across the commonwealth last month. This is 974 fewer sales… Read More

Three Multifamily Market Trends from the Second Quarter of 2024

By Sejal Naik - July 16, 2024

Each quarter, through its Multifamily Market report, the research team at Virginia REALTORS® analyzes the trends and changes in the multifamily market. Here, we share the key highlights… Read More

Takeaways From the JCHS 2024 State of the Nation’s Housing

By Dominique Fair - July 15, 2024

The Joint Center for Housing Studies from Harvard University released this year’s State of the Nation’s Housing report highlighting the impact today’s market is having on both homeowners… Read More