When Fixed-Rate Mortgage Rates Go Up, Adjustable-Rate Mortgages Rise in Popularity

December 28, 2023

The interest rate for a 30-year fixed mortgage has been on the downward trend for the past few weeks after peaking at an almost 23-year high in October 2023. As of December 14, 2023, the average 30-year mortgage rate had simmered down to 6.95 percent. In response to such changes in the fixed-rate mortgage rates, what happens to the share of adjustable-rate mortgages in the market?

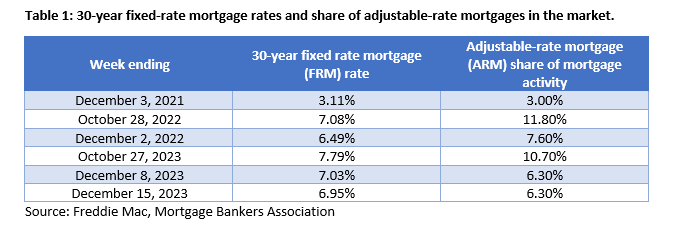

In table 1, we list the 30-year fixed-rate mortgage rate and the share of adjustable-rate mortgages at different points in time. As can be seen, when fixed-rate mortgage rates go up, the share of adjustable-rate mortgages goes up as part of the overall mortgage market activity. Conversely, when fixed-rate mortgage rates go down, the share of adjustable-rate mortgages goes down as well. In the two-year period from December 2021 through December 2023, the average 30-year fixed-rate mortgage (FRM) rate more than doubled. In the same period, adjustable-rate mortgages (ARM) gained an increased interest as seen in their rising share of total mortgage market activity.

In an adjustable-rate mortgage, the interest rate is set for a period, and then adjusts over time based on the market. Initially, ARMs typically have lower interest rates than FRMs and allow home buyers to experience significant monthly savings in the beginning. For example, a 5/1 ARM has a fixed rate for the first five years, followed by a variable rate that adjusts every year for the rest of the loan term. People opting for an ARM hope that rates will go down in the future and prioritize flexibility instead of predictability that comes with a fixed rate mortgage. As FRM rates went up over the past couple of years, ARMs became more appealing to home buyers who want to keep their initial mortgage costs as low as possible. However, it is worth noting that there is no guarantee that rates will drop in the future. Consequently, a homeowner could end up spending more on monthly payments during the loan term. This will also require a more frequent reassessment of their budget that goes towards home payments.

To summarize, when fixed rates are low, ARMs become less popular. While, as fixed rates go up, ARMs regain popularity. In the coming weeks, we expect the fixed rate mortgage rates to continue their downward trajectory. However, it is always prudent to stay informed about the different mortgage options available for potential home buyers and determine how to best utilize them based on the current interest rate environment.

For more information on housing, demographic and economic trends in Virginia, be sure to check out Virginia REALTORS® other Economic Insights blogs and our Data page.

You might also like…

What the New Federal Housing Law Means for Virginia Real Estate Professionals

By Sejal Naik - August 3, 2026

After years of back-and-forth in Congress, the 21st Century ROAD to Housing Act is now law. Passing with big bipartisan majorities, it took effect on July 11,… Read More

Key Takeaways: June 2026 Virginia Home Sales Report

By Virginia REALTORS® - July 22, 2026

Key Takeaways The June housing market was busy around the Commonwealth. There were 11,598 closed sales statewide, which is 823 more than last June, a 7.6% influx. Halfway… Read More

Three Multifamily Market Trends from the Second Quarter of 2026

By Sejal Naik - July 15, 2026

Each quarter, through its Multifamily Market report, the research team at Virginia REALTORS® analyzes the trends and changes in the multifamily market. Here, we share the key insights… Read More